The Financial Conduct Authority (FCA) has issued a second consultation [1] as it seeks to refine its new Consumer Duty proposal, aimed at providing a higher level of consumer protection in retail financial services.

Martin Kisby, Director of Compliance, EQ Credit Services, looks at the progress to date on this important initiative, and previews what businesses can expect when it comes into force over the summer.

Further consumer protections to drive cultural change

The FCA’s aim for the new Duty remains the same - to bring about “a higher level of consumer protection in retail financial markets, where firms compete vigorously in the interests of consumers”.

The current consultation provides more detailed proposals for the Consumer Duty, including draft Handbook rules, cost-benefit analysis, and draft non-Handbook guidance to assist firms in preparing for its introduction. Whilst the FCA confirmed that the Consumer Duty would not apply retrospectively to past business, the new guidance will apply on a forward-looking basis to existing products or services, which are either still being sold to customers, or closed products or services that are not being sold or renewed.

Three key aims for the duty are:

- Firms must consistently place consumers’ interests at the centre of their businesses by going beyond compliance with specific rules, to focus on delivering good outcomes for consumers

- That competition is effective in driving market-wide benefits, as firms compete to attract and retain customers based on high standards and innovation, in pursuit of good consumer outcomes

- For consumers to get products and services which are fit for purpose, provide fair value, and that they fully understand and are supported in using them.

The FCA’s view is that the initiative will help to drive a healthy and successful financial services system, in which firms can thrive, and consumers can make informed choices about financial products and services.

In particular, the FCA wants to achieve the following:

- Explicitly setting a higher standard of care across all retail markets, informed by its work on behavioural biases and vulnerability

- Extending rules focused on product governance and fair value, which already exist in certain sectors, to all sectors

- Focusing on matters of market practice (e.g. sludge practice) that interfere in consumer decision making and, by doing so, cause harm

- Ensuring firms consider the needs of their customers – including those with characteristics of vulnerability – and how they behave at every stage of the product or service lifecycle

- Requiring all firms to focus on good customer outcomes and whether those outcomes are met.

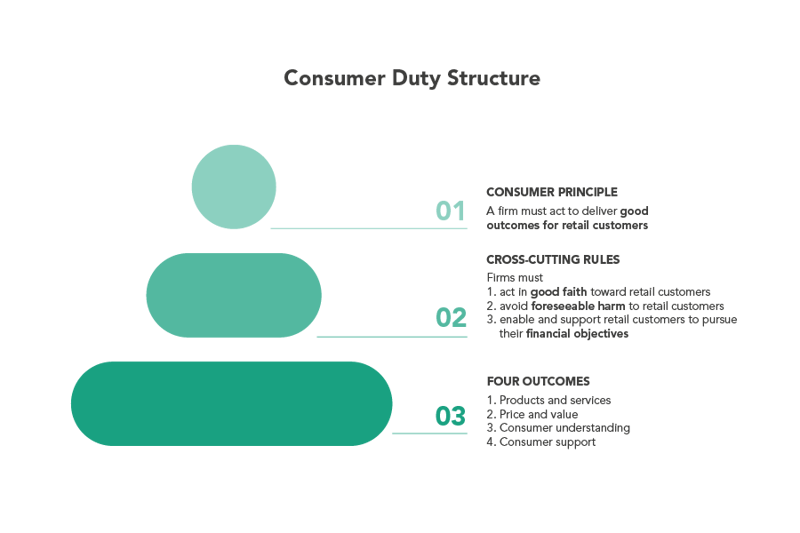

The three elements of the Consumer Duty – Principles, rules and outcomes

The FCA has identified three elements that make up the Consumer Duty, as illustrated below:

The New Consumer Principle

“A firm must act to deliver good outcomes for retail customers.”

The Consumer Principle is intended to underpin and drive change in culture and conduct that the FCA expects to see in firms, and it reflects the overall standard of behaviour expected from firms.

The introduction of the Consumer Duty does bring into question the future roles of Principles 6 and 7, which cover treating customers fairly and customer communications respectively. With a higher standard for both Principles now covered by the Consumer Duty, the FCA proposes to disapply both Principles where the Consumer Duty applies. Principle 6 and 7 will, therefore, continue to apply only to conduct outside the scope of the Consumer Duty, e.g. certain SMEs and wholesale businesses.

Cross-cutting rules

The cross-cutting rules which the FCA are proposing require firms to:

- Act in good faith towards retail customers

- Avoid causing foreseeable harm to retail customers

- Enable and support retail customers to pursue their financial objectives.

The FCA considers that the cross-cutting rules are an important component of the Consumer Duty and their role is to:

- Develop the FCA’s overarching expectations for behaviour through three common themes that apply across all areas of firm conduct

- Set out how firms should act to deliver good outcomes

- Inform and help firms interpret the four outcomes.

The four outcomes

The Four outcomes set out below, give more detailed expectations for the key elements of the firm-consumer relationship.

1) Products and services outcome

The FCA sets out that firms are manufacturers or co-manufacturers if they create, develop, design, issue, operate, underwrite, or have a decision-making role in a product or service. Where products or services were poorly designed or distributed widely to consumers, for whom they were not designed, the FCA has identified consumer harm.

Consumers are only able to pursue their financial objectives and avoid foreseeable harm when products and services are fit for purpose. The FCA sets out that firms, acting in good faith, should design and distribute products and services to meet this aim. Therefore, the FCA’s products and services outcome rules are central to firms acting to deliver good outcomes.

They set out a range of requirements, including the need for relevant firms to:

- Ensure that the design of the product or service meets the needs, characteristics and objectives of consumers in the identified target market

- Ensure that the intended distribution strategy for the product or service is appropriate for the target market

- Carry out regular reviews to ensure that the product or service continues.

2) Price and value outcome

The FCA recognise that consumers experience harm where they do not get value for money, and which is unlikely to be consistent with customers realising their financial objectives. Firms cannot be acting in good faith if they are knowingly selling poor value products or services.

Firms are not expected to only offer products and services at a low price, however, the FCA expects firms to consider price when assessing fair value, but not at the expense of other factors. Fair value is about more than just price and it needs to be considered in the round. The benefits consumers can reasonably expect from a product or service should be assessed against the price.

The Consumer Duty aims to tackle factors that can result in products or services which are unfair or poor value, such as unsuitable features that can lead to foreseeable harm or frustrate the customer’s use of the product or service, or poor communications and consumer support.

3) Consumer understanding

The FCA wants firms to support their customers by helping them to make informed decisions about financial products and services. To do this, consumers must be given the information they need, at the right time, and have it presented in a way they can understand.

The consumer understanding outcome rules build on and go further than, Principle 7 by requiring firms to:

- Support their customers’ understanding, by ensuring that their communications meet the information needs of retail customers, are likely to be understood by the average customer, and equip them to make decisions that are effective, timely and properly informed

- Ensure they communicate information in a way that is clear, fair and not misleading

- Tailor communications, considering the characteristics of the retail customers intended to receive the communication – including any characteristics of vulnerability, the complexity of products, the communication channel, and is accurate, relevant, and provided on a timely basis

- Tailor communications to meet the information needs of individual customers and check the customer understands the information. Test, monitor and adapt communications to support understanding and good outcomes for retail customers.

4) Consumer support

The FCA expects firms to provide the support that meets their customers’ needs. The support firms provide should enable consumers to realise the benefits of the products and services they buy, pursue their financial objectives, and ensure that they can act in their own interests.

The FCA’s consumer support outcome rules go further than the existing rules, in relation to the support firms provide their customers. It should also be read in conjunction with other rules that cover specific elements of the servicing of customers, e.g. Dispute resolution: Complaints (DISP) rules.

They require firms to:

- Consider the support their customers need, and make sure their customer service meets those needs

- Support their customers in a way that takes their needs into account, such as not designing processes with unreasonable barriers that prevent consumers from realising the benefits of the product or service

- Monitor the quality of the support they are offering, looking for evidence that may indicate areas where they fall short of the outcome, and act promptly to address these

- Ensure they do not disadvantage groups of customers, including those with characteristics of vulnerability.

Raising consumer standards and encouraging responsibility

The FCA considers that the Consumer Duty should have a positive impact for all consumers, including those in vulnerable circumstances, and as such, raises the standard expected from firms across the board.

Where the Consumer Duty rules reference consumers in vulnerable circumstances, these are in line with FCA guidance on the fair treatment of vulnerable customers. The FCA’s proposed rules embed consideration of these consumers at every stage of the customer journey.

This guidance on the fair treatment of vulnerable customers will remain relevant to firms in considering their obligations under the Consumer Duty, and failure to act in accordance with existing guidance on Principles 6 and 7, would be likely to breach the Consumer Duty.

However, the FCA clearly states that the Consumer Duty does not remove consumers’ responsibility for their choices and decisions. Firms have a vital role to play in enabling and empowering consumers to take responsibility for their own actions and decisions. However, consumers can only be expected to take responsibility for their actions, when they can trust that the range of products and services, they choose from are designed to meet their needs, and offer fair value.

Where consumers need assistance to understand products and services, this should be provided. The FCA and consumers should have confidence that firms will act in a way that helps, rather than hinders, their decision-making ability in line with their needs and financial objectives.

Outcome-driven oversight

In determining the success of the new Consumer Duty, the FCA sets out that firms will need to identify relevant sources of data, to enable them to assess whether the outcomes that their customers are experiencing are consistent, with their obligations, under the new guidance.

Through the monitoring of consumer outcomes, the FCA expects firms to:

- Identify and manage any risks to good outcomes for consumers.

- Spot where consumers are getting poor outcomes, and understand the root cause.

- Have processes in place to adapt and change products/services or policies/practices to address any risks or issues as appropriate.

- Be able to demonstrate how they have identified and addressed issues leading to poor outcomes. All senior managers are responsible for ensuring that the business of the firm complies with the requirements of the Consumer Duty on an ongoing basis. An assessment of whether a firm is delivering good outcomes for its customers, consistent with the Consumer Duty, should be reviewed and approved by a firm’s board, at least annually.

The FCA sets out that the assessment should include:

- The results of the monitoring that the firm has undertaken, to assess whether their products and services are delivering expected outcomes in line with the Consumer Duty

- New and emerging risks to good outcomes for consumers

- Any evidence of poor outcomes, and an evaluation of the impact and the root cause

- Actions taken to address any risks or issues

- How the firm’s future business strategy is consistent with acting to deliver good outcomes under the Consumer Duty.

A firm’s Board should agree the action required to address any issues which are impacting the firm’s ability to deliver good outcomes and agree whether any changes to the firm’s future business strategy are required, before sign off.

The assessment is expected to be provided on request of the FCA and will form part of the evidence used to assess a firm’s compliance with the Consumer Duty.

Preparing for the consumer-focussed future

With the FCA consultation closing on 15 February, and a new policy statement expected by the end of July, businesses can start planning now for any changes they need to make to their customer-facing processes, services and products.

In particular, the four outcomes should drive current thinking on what the FCA are looking for from their Consumer Duty policy statement and guidance.

Whatever Your Customer Challenges, Whenever Your Customers Challenge

EQ improves the performance of customer service and complaints operations. Meeting regulatory and customer promises with exceptional results.